The financial math is unforgiving. With U.S. median gross rent sitting at $1,487 per month according to 2024 Census data, most renters have very little room between "employed" and "behind on rent." Yet income protection — the insurance mechanism designed to bridge exactly this gap — rarely gets discussed in renter-focused conversations.

This article explains what tenant income protection is, why it matters practically for both renters and landlords, and what happens when it's missing.

Key Takeaways

- Tenant income protection replaces a portion of a renter's income when illness or injury prevents them from working — keeping rent payments on track

- 42% of renters couldn't cover three months of expenses if their primary income stopped, per 2024 Federal Reserve data

- Renters avoid eviction risk; landlords avoid arrears and costly vacancy gaps

- Policies typically replace 50–70% of income, with benefits lasting 12 months to retirement age

- It's not the same as rent guarantee insurance — different product, different purpose, different policyholder

What Is Tenant Income Protection?

Tenant income protection is a disability or income protection insurance policy held by a renter, designed specifically to ensure rent keeps getting paid when work stops.

In the U.S., this isn't sold as a single named product. Instead, it functions through two types of coverage:

- Short-term disability insurance — covers a temporary inability to work, typically up to 3–6 months

- Long-term disability insurance — covers extended periods when recovery takes much longer

After a waiting period, monthly benefit payments replace a percentage of the renter's pre-disability earnings. The practical purpose is straightforward: keep rent paid through a health setback, so a medical issue doesn't snowball into a housing crisis.

Who Needs It Most

Employer-provided disability coverage is far from universal. March 2025 Bureau of Labor Statistics data shows only 44% of private industry workers had access to short-term disability insurance, and just 37% had long-term disability access. For part-time workers, short-term disability access dropped to 11%.

That leaves a large share of renters — part-time workers, gig workers, freelancers, and self-employed individuals — with no automatic income replacement if they can't work.

Key Advantages of Tenant Income Protection

For renters without savings buffers, income protection is less about planning and more about staying housed when the unexpected hits.

Housing Stability During Income Disruption

The core benefit is direct: when a renter can't work, income protection replaces a portion of their earnings so rent payments continue.

After an elimination period (typically 1–4 weeks for short-term policies, up to 90 days for long-term), monthly benefit payments begin. The renter receives cash (not a payment made on their behalf) and can allocate it across rent, utilities, food, and medical expenses as needed.

The stakes are high for renters with little financial cushion:

- Renters typically fall into arrears after just one to two missed months, triggering eviction proceedings that damage credit and disrupt employment simultaneously

- Federal Reserve 2024 data found 42% of renters couldn't cover three months of expenses by any means if their primary income stopped

- Harvard's Joint Center for Housing Studies reported that renter households earning under $30,000 had median cash savings of just $300 in 2022 — less than one week's rent at median rates

- The monthly cost of an income protection premium is a fraction of what eviction, temporary housing, or debt accumulation costs

This protection matters most for renters spending a high share of income on housing, single-income households, and anyone without employer-provided sick pay.

Reduced Arrears and Eviction Risk — For Landlords Too

Tenant income protection isn't only a renter's tool. When a tenant carries it, landlords benefit directly: rent arrives consistently even if that tenant faces a health crisis or job loss.

The scale of the arrears problem is real. The same Federal Reserve data shows 21% of renters were behind on rent at some point in 2024. When a tenant defaults, the landlord's costs go well beyond lost rent . The National Apartment Association estimates the average eviction costs a landlord $6,767, including legal fees, court costs, lost rent, turnover, and re-letting expenses.

- Eviction Lab tracked 1.23 million eviction cases in monitored locations in 2025, roughly one filing per 13 renter households

- A tenant with income protection in place converts a potential arrears scenario into a reliable, low-risk tenancy

- Landlords with a single rental property face the sharpest exposure: one missed rent cycle can immediately pressure mortgage payments or maintenance budgets

Proactively encouraging tenants to carry income protection is a practical risk management step, not just a goodwill gesture.

Financial Resilience Without a Debt Spiral

A less visible but equally important advantage: income protection lets renters recover fully without being pushed back to work too early or forced to borrow against future earnings.

Without this buffer, the typical pattern looks like:

- Illness or injury stops income

- Renter charges rent to a credit card or takes a personal loan

- Returns to work before fully recovered to avoid further debt

- Debt from the health event persists for months or years afterward

Federal Reserve 2024 data found 25% of renters didn't pay at least one bill in full in the prior year, and late fees reached an average of $85 by late 2024. These aren't rare edge cases. They're the predictable result of thin financial margins meeting unexpected income loss.

Income protection short-circuits this cycle. A renter who exits a health crisis without accumulated debt is far better positioned to maintain tenancy and rebuild savings. For self-employed renters and freelancers with no employer sick pay, that buffer can be the difference between a temporary setback and a prolonged financial hole.

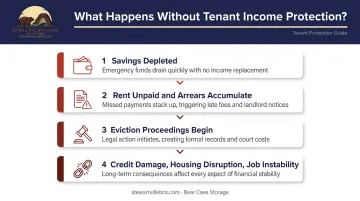

What Happens When Tenant Income Protection Is Missing

The sequence is predictable once income stops:

- Savings run out within weeks

- Rent goes unpaid and arrears accumulate

- Eviction proceedings begin

- Credit damage, housing disruption, and job instability follow simultaneously

For landlords, an unprotected tenant in financial crisis triggers a reactive spiral: pursuing missed payments, initiating legal proceedings, managing vacancy, and absorbing turnover costs. All of it avoidable if the risk had been addressed earlier.

There's also a practical downstream reality that doesn't get discussed much: when renters face eviction or must vacate suddenly, their belongings often have nowhere to go. Finding new housing takes time, and most people can't move furniture and household goods directly from one home to the next on short notice.

Bear Cave Storage, a locally owned facility serving Rochester and Stewartville, Minnesota, regularly works with renters navigating exactly this kind of gap. Flexible month-to-month terms and 24/7 gated access make it a practical bridge option while longer-term housing gets sorted out.

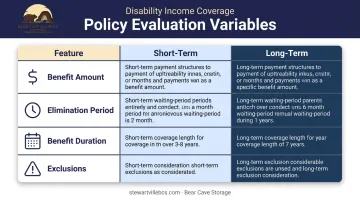

How to Choose Tenant Income Protection Effectively

When evaluating policies, renters should focus on four variables:

| Feature | What to Know |

|---|---|

| Benefit amount | Short-term policies typically replace 50–80% of wages; long-term policies often replace 50–60% |

| Elimination period | Short-term: often 1–30 days. Long-term: often 90 days. Shorter periods cost more |

| Benefit duration | Short-term: 12–52 weeks (median 26 weeks). Long-term: years, or until retirement age |

| Exclusions | Pre-existing conditions may be excluded or limited — read these clauses carefully |

Coverage should match actual rent obligations. A renter spending 40% or more of their income on housing needs a shorter elimination period and a higher benefit amount than someone with lower housing costs and a larger savings buffer.

Other factors worth checking:

- Self-employed renters can obtain individual disability insurance but should expect to provide two years of tax returns and potentially pay higher premiums

- Pre-existing conditions don't automatically disqualify an applicant, but may result in exclusions for related claims — some exclusions can be reviewed after 1–3 years if the condition is managed

- Compare multiple policies before committing; terms vary significantly between carriers

Conclusion

Tenant income protection converts a volatile risk into a managed financial outcome. When illness or injury strikes, it keeps rent paid and renters housed — without the debt spiral, credit damage, and housing instability that follow an unprotected income gap.

A policy secured before a health event costs less and covers more than any reactive scramble after the fact. For renters whose monthly rent represents a large share of their income, that timing difference alone can determine whether a medical setback becomes a financial crisis — or doesn't.

Frequently Asked Questions

Is it worth paying for income protection insurance?

For renters, yes — particularly those without employer sick pay. Missing even one or two months of rent due to illness can trigger arrears and eviction proceedings. The monthly premium cost is typically far lower than the combined financial and personal cost of housing instability.

Does income protection cover osteoarthritis?

Most policies can cover musculoskeletal conditions including osteoarthritis if the condition prevents the policyholder from working and the policy's definition of disability is met. Coverage depends on whether the condition is classified as pre-existing at the time of application — exclusions are possible but not universal.

What is the difference between tenant income protection and rent guarantee insurance?

Tenant income protection is held by the renter and pays them a portion of their income when they can't work. Rent guarantee insurance is held by the landlord and covers unpaid rent if a tenant defaults. They serve entirely different parties and should not be confused with one another.

How long does tenant income protection coverage typically last?

Short-term policies typically pay out for 12–52 weeks per claim; long-term policies can provide benefits until retirement age. The right choice depends on the renter's financial obligations, savings buffer, and how long they could realistically manage on reduced income.

Does tenant income protection cover self-employed renters?

Yes — self-employed renters can obtain individual disability insurance through private carriers. Expect to provide proof of at least two years of self-employment and tax returns. Premiums may be higher and underwriting more rigorous than group employer plans.

What does tenant income protection typically not cover?

Most policies exclude pre-existing conditions diagnosed before the application date, self-inflicted injuries, and unemployment due to voluntary resignation or redundancy. Policies also generally won't pay out during a waiting (deferral) period — typically 4 to 13 weeks — so renters with minimal savings should factor that gap into their planning.