The impulse to cancel and save money is understandable. But according to Minnesota DPS crash data, the state has 304,433 registered motorcycles — and virtually none of them are on the road in January or February. That's a lot of parked bikes, and parked doesn't mean risk-free.

This article covers the real, practical case for keeping motorcycle storage insurance active during the off-season — what it costs, what it covers, and what you lose if you drop it.

Key Takeaways

- Comprehensive coverage protects a stored bike against theft, fire, vandalism, and weather damage year-round

- Canceling entirely creates a coverage gap that can raise your premiums and complicate reinstatement in spring

- Lay-up or storage endorsement policies let you drop riding-related coverages (liability, collision) while keeping comprehensive active at a lower cost

- Storage facility insurance covers the building, not your motorcycle

- Enclosed, secured indoor storage reduces risk and can support better coverage terms

What Is Motorcycle Storage Insurance

Motorcycle storage insurance isn't a separate product you buy at a dealer. It's the coverage that stays active on your bike while it sits — protecting against risks that have nothing to do with riding.

In practice, it usually takes one of two forms:

- A reduced or modified standard policy — where liability and collision are lowered or paused, but comprehensive remains active

- A lay-up endorsement — a formal policy adjustment offered by some insurers (Dairyland and Foremost both document this publicly) that structures coverage for a non-riding period

If your bike is stolen, catches fire, or gets damaged in a storage building collapse during a January ice storm, the insurer absorbs the loss — not you. That protection is exactly what storage coverage is built for, and why simply canceling your policy for the winter can leave you exposed.

Key Advantages of Keeping Your Motorcycle Insured During Storage

Three advantages matter here: financial protection, avoiding costly policy gaps, and controlling what you actually spend during the off-season.

Advantage 1: Protection Against Theft, Fire, and Weather Damage

Comprehensive coverage is what protects a parked motorcycle. According to Progressive, it covers theft, vandalism, weather-related damage, fire, and animal collisions — exactly the risks a stored bike still faces.

Theft is not just a warm-weather problem. The NICB reported 54,736 motorcycles stolen in 2022 — a 7% increase from the prior year, averaging roughly 4,561 stolen per month. The NICB also specifically advises owners to lock motorcycles even when stored in a garage, which tells you something about the actual risk level during storage.

The financial exposure is real:

| Motorcycle | Category | MSRP |

|---|---|---|

| Honda Rebel 500 | Mid-range cruiser | $6,799 |

| Harley-Davidson Street Glide | Premium touring | Starting at $24,999 |

Comprehensive coverage during storage typically costs a fraction of either figure annually. If a $7,000 bike gets stolen in February with no coverage in place, you absorb the full loss.

Riders storing bikes in shared facilities, garages near other vehicles, or any area where the bike sits stationary for months face the highest exposure. Minnesota's long off-season makes that window predictable — and long.

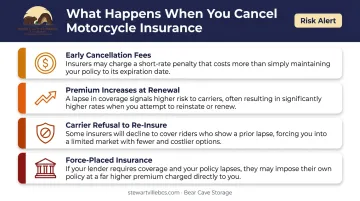

Advantage 2: Avoiding Coverage Gaps, Cancellation Penalties, and Premium Increases

Canceling coverage entirely — rather than adjusting it — creates a gap in your insurance history. Most insurers treat that gap as a risk signal when you reapply in spring.

The compounding effects:

- Early cancellation fees reduce any refund you'd expect; short-rate cancellation means the insurer keeps more than a prorated share

- Premium increases at renewal are a documented risk; both Progressive and Dairyland note that lapses can affect future rates

- Refusal to re-insure is possible if a carrier views annual cancellation as a pattern

- Force-placed insurance kicks in for financed bikes — when a lender buys coverage on your behalf after yours lapses, it's typically more expensive and offers less protection than a policy you'd choose yourself

The riders most exposed here are those with financed motorcycles, anyone who has built a multi-year claims-free record, and riders who've already seen rates rise after a previous lapse. Maintaining even a minimal storage-period policy protects that record.

Advantage 3: Cost Savings Through Lay-Up Policies

You don't have to choose between full coverage and no coverage. Lay-up policies give you a practical middle ground.

During the storage period, the insurer removes or reduces liability, collision, and medical payments — the coverages tied to active riding — while keeping comprehensive in place. Some providers, including Dairyland, add a "sunny day clause" that grants one day of liability coverage during a lay-up period for an unexpected warm-weather ride.

Illustrative cost context (based on ValuePenguin benchmarks — actual rates vary by insurer, bike, and location):

- Full-coverage motorcycle insurance: roughly $10–$139/month depending on coverage level and profile

- A lay-up policy removes the most expensive riding-related coverages, reducing the seasonal cost significantly

- Increasing your comprehensive deductible alone may lower premiums by up to 35%

Riders who switch to a storage endorsement for 4–5 months and back to full coverage in spring consistently spend less annually than those who cancel and restart — without the hassle of reinstating a policy each spring.

If you're in a northern state with a 4–6 month off-season, own a higher-value bike, or simply want to cut costs without the gap, a lay-up policy is worth a direct conversation with your insurer.

What Happens When Coverage Is Dropped During Storage

Going uninsured during the off-season creates several concrete problems:

- Theft, fire, or damage becomes a total out-of-pocket loss — there's no claim to file and no recovery path.

- Financed bikes carry lender obligations. Dropping coverage without notifying your lender can trigger force-placed insurance — purchased by the lender, billed to you, at a higher rate with less protection.

- One warm day undoes the plan. Take the bike out on a 50-degree February afternoon with no liability coverage and you're fully exposed.

- The savings rarely hold long-term. Reinstatement fees, higher renewal premiums, and potential carrier refusal often mean riders pay more over two or three years than they saved by canceling for one winter.

Some riders assume the storage facility fills that gap — it doesn't. Storage facility insurance does not cover your motorcycle. Public Storage explicitly states customers are required to carry their own insurance on stored goods. MiniCo, a self-storage insurance provider, confirms the same — lease agreements make tenants responsible for their own property. The facility's coverage protects the building, not what's inside.

How to Get the Most Value from Motorcycle Storage Insurance

Getting the most out of a storage policy comes down to preparation — before you park the bike and when you're ready to ride again. These four steps cover the key moments where most riders leave value on the table:

Call your insurer before storing — ask specifically about lay-up or storage endorsement options. Confirm comprehensive coverage stays active and whether the policy has requirements about where the bike is stored, such as a locked unit or enclosed space.

Match your storage environment to your coverage terms — insurers generally treat fully enclosed, secured storage as lower risk than outdoor or unsecured options. This can support better coverage terms and a reduced risk profile. Bear Cave Storage's indoor motorcycle units in the Stewartville and Rochester area are fully enclosed with drive-up access and 24/7 gated security.

Document before you store — take dated photos of the motorcycle, record the VIN and any custom equipment, and keep a copy of your insurance declarations page with your storage paperwork. This makes any future claim much easier to process.

Review coverage at the start of riding season — don't let a lay-up policy auto-renew at the wrong level. Confirm your policy reflects active riding before you leave the lot.

Conclusion

Motorcycle storage insurance exists for the months when you assume nothing will happen. A bike stolen from a storage unit in January is still gone. A fire in an adjacent bay doesn't wait for May. Off-season doesn't mean risk-free.

Riders who maintain continuous coverage at a storage rate protect their investment, preserve their insurance history, and come back to riding season without the friction and costs that follow a lapse. The lay-up model makes that practical: lower premiums during storage months, full protection on the risks that actually matter, and no gaps to explain when you're ready to ride again.

Frequently Asked Questions

What kind of motorcycle storage insurance do I need?

Comprehensive is the most important coverage to keep active during storage — it covers theft, fire, vandalism, and weather damage. Many insurers offer a lay-up or storage endorsement that removes liability and collision to reduce your premium while keeping comprehensive in place.

Can I cancel my motorcycle insurance while my bike is in storage?

It may be legal if the bike isn't registered or ridden, but canceling entirely risks a coverage gap, cancellation fees, and higher premiums when you reinstate. It also leaves the bike completely unprotected from theft, fire, or damage during storage.

Does my storage facility's insurance cover my motorcycle?

Storage facility insurance covers the building — not the vehicles or items inside it. You're responsible for carrying your own coverage to protect the motorcycle itself.

What is a lay-up policy for motorcycles?

A lay-up policy pauses riding-related coverages — liability, collision, and medical payments — while keeping comprehensive coverage active. The result is a lower off-season premium without leaving the bike unprotected.

Does storing my motorcycle indoors vs. outdoors affect my insurance?

Most insurers treat indoor, enclosed storage as lower risk, which can mean lower premiums or broader coverage options. Outdoor or unsecured storage increases theft and damage exposure and can trigger policy exclusions or higher costs.

Will my homeowners or renters insurance cover my motorcycle in storage?

No. Standard homeowners and renters insurance does not extend to motor vehicles. A separate motorcycle insurance policy is required to protect the bike from theft, fire, or damage — whether it's stored at home or at a facility.